Basis Commodities – Australian Crop Update – Week 35 2022

Market Update

Australian cash markets remain relatively quiet. Buyers are well covered on the old crop positions while farmers, guided by local farm consultants and a wet medium-term forecast, are showing little interest in chasing markets lower for new crop. Australia is on track for another 32MMT plus national wheat crop, 12MMT or more of barley and more than 6MMT of canola. This will result in stock builds in all crops as we simply do not have enough export logistics to move that crop, particularly if we get another wet summer as forecast. In addition, we are seeing intense competition from Russian CFR sellers into the Middle East, East Africa, and Asia.

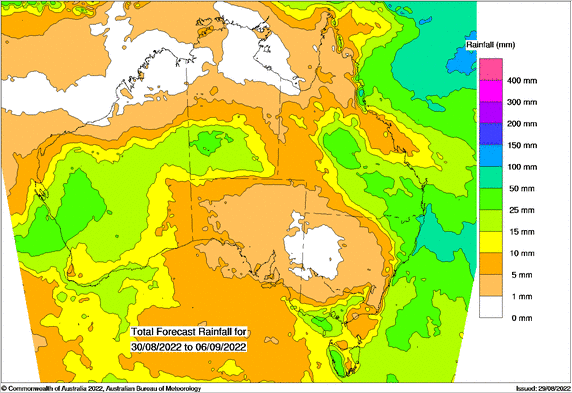

Widespread rain across Western Australia (WA) will help to lock in another massive WA grain harvest in 2022. Recent rain across other states is also lifting national production prospects, although New South Wales (NSW) could do with a breather. WA crop conditions aren’t quite as good as last year at the same time, but they are not far behind it. Most of the countries cropping regions are well positioned heading into spring, where the BOM is forecasting wetter than normal weather. South Australia’s (SA) Eyre Peninsula is the best in a decade as is Victoria (VIC). Other parts of SA are improving with the recent rain and warming temps which is allowing crops to grow. The southern third of NSW is well above average and the northern 25% is well positioned for well-above average yield. The rest of the state is improving as temperatures climb. Queensland (QLD) crops are also well positioned for above average yields.

The bottom line is, a 32MMT plus crop wheat crop justifies another year of low basis levels. Not to the same extent perhaps as the past six month when global cash markets, including Australia, ignored the massive runup in U.S. futures, but a continuation with the current low levels needed to push Aussie wheat exports deep into the western hemisphere, which is needed to shift 24-25MMT of wheat exports.

Last week we passed on our analyst’s forecasts for Australia’s wheat, barley, and canola balance sheets. Interestingly we are using national 2021/22 wheat exports at 27.5MMT, barley export at 8.2MMT and canola exports of 5.5MMT. The barley exports are below USDA’s 9.0MMT which looked optimistic from the start. This leaves wheat carry out stocks at 4.1MMT, barley at 2.3MMT and canola at 0.6MMT. The most notable feature of the carryover stocks is that wheat and barley stocks in WA are building on the back of last year’s massive crop. WA has 2.5MMT of the 4.1MMT national wheat stocks and 0.8MMT of the 2.3MMT national barley ending stocks at Oct 1.

Ocean Freight

Despite an avalanche of negative sentiment last week, the ocean freight market in Southeast Asia managed to buck the trend and held up well. Although that positive sentiment was starting to wane by the end of the week. Elsewhere, it has been a desperate week – Panamax rates in both oceans leading the charge to the bottom with older sub-index types staring at a sub $10k market soon if things don’t pick up. The disparity between Ultramax rates touching mid/low $20k’s pd and Panamaxes is stark and will surely rebalance itself. Any cargo over 40KMT that doesn’t need gear and can fit 200+ m loa is going to be a Panamax lift on these rates.

Australian Dollar

The Australian dollar is weaker this morning (29/8/22) trading just below 69 US cents. On Friday the AUD was one of the hardest hit amidst the sharp pullback in risk appetite falling 1.2% against the USD after the Federal Reserve Chair Jerome Powell delivered his much-anticipated keynote speech at Jackson Hole sending an unambiguous message that the Fed is committed to getting inflation back to the 2% target. From a technical perspective, the AUD/USD’s first support level would be at 0.6855. Once cleared, the next stop would be 0.6810, followed by 0.6770. Any resistance will be seen at 0.6960 followed by 0.6990.

The post Basis Commodities – Australian Crop Update – Week 35 2022 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.

Newsletter Signup

Quick Links

Basis Commodities Pty Ltd

PO Box 340, Northbridge

NSW 1560, Australia

Basis Commodities Consulting DMCC

PO Box 488112

Dubai, UAE

Copyright © 2024 Pty Ltd. All rights reserved.

site by mulcahymarketing.com.au