Basis Commodities – Australian Crop Update – Week 6 2022

Market Update

Domestic market price changes in the past week were variable and reflective of the nearby exporter coverage. Most of the focus is on logistics with exports now running at maximum capacity and most exporters are well sold through to June.

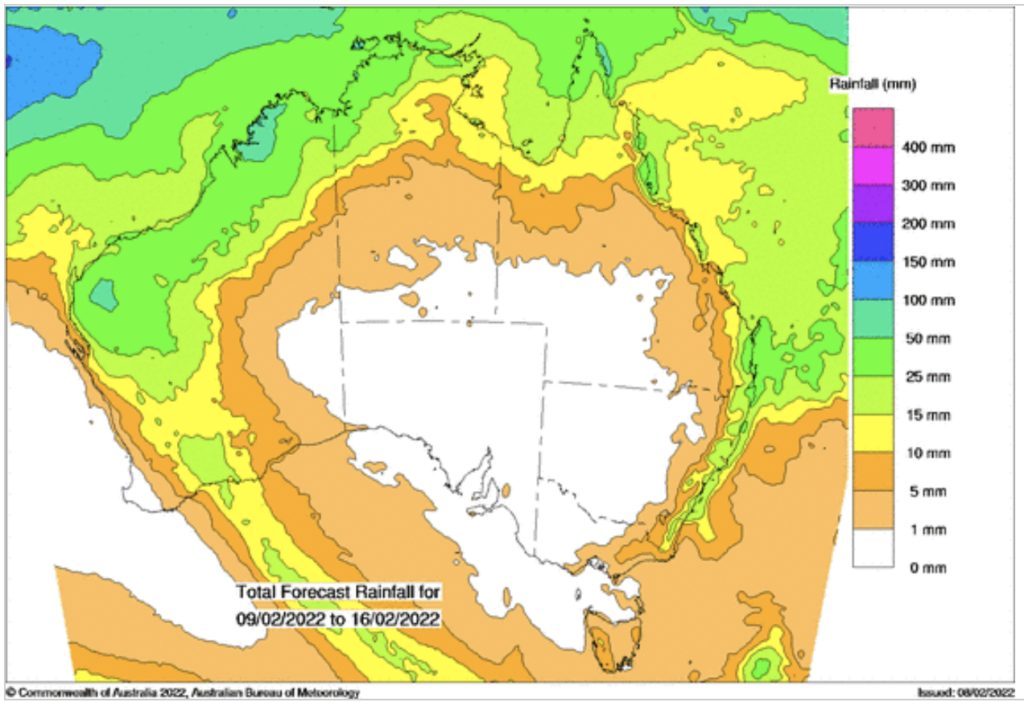

Shipping is at capacity and loading stems are seeing some slippage in the business ports of Western Australia and New South Wales as logistics, weather and bushfires have an impact. Even though the combined February wheat, barley and canola loadings are up to 4.3MMT, some of this won’t be loaded until March.

Grain exports in December combined for a total of about 3.5MMT for the month and January should be at 4.0MMT or more across wheat, barley, canola and other grains.

Interestingly, given the political tensions, China was the major wheat destination accounting for 715KMT, or about a third of all wheat shipments in December with Indonesia the second biggest.

Barley exports topped 1MMT in December.

Ocean Freight

As most of the Asian market returned to work after the Lunar New Year holidays, the ocean freight market, or more particularly the owners, were looking to start the year of the tiger with higher rates. However, charterers are currently resisting that assumption. From here, the market looks to be at a pivot point but with a lot of vessels committed to the backhaul to the Atlantic, we feel there may be a risk of a tonnage short emerging in Southeast Asia. It is more apparent on smaller sizes where tonnage lists are surprisingly short, but a quick glimpse at all the Baltic indices shows positivity in most areas.

Australian Dollar

The gains in commodities were supportive for the AUD, however the USD was much stronger after the U.S. employment data, which saw AUD/USD down 1% on the day. The AUD starts the new week below 0.7100.

Last week the Reserve Bank of Australia (RBA) decided to maintain rates at record lows and its monetary policy unchanged in its February meeting. The RBA statement indicated that “the Board judged that it is too early to conclude that inflation is sustainably in the target range,” a dovish stance that prevented the Australian dollar from rallying. From a technical perspective, we continue to expect support to hold on to moves approaching 0.6970. A breach of these levels would open the door to further Australian dollar weakness.

The post Basis Commodities – Australian Crop Update – Week 6 2022 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.

Newsletter Signup

Quick Links

Basis Commodities Pty Ltd

PO Box 340, Northbridge

NSW 1560, Australia

Basis Commodities Consulting DMCC

PO Box 488112

Dubai, UAE

Copyright © 2024 Pty Ltd. All rights reserved.

site by mulcahymarketing.com.au