Basis Commodities – Australian Crop Update – Week 18, 2023

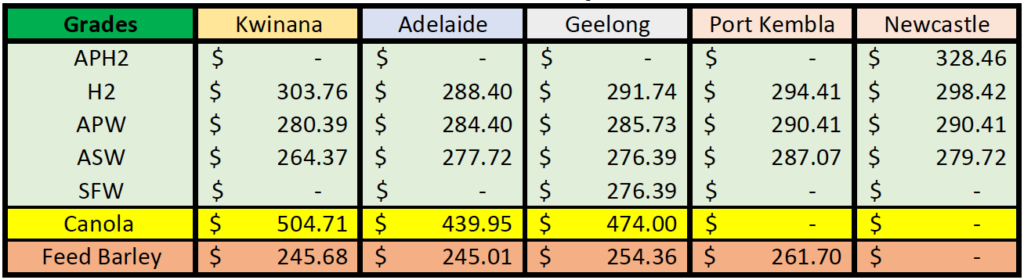

2022/2023 Season (New Crop) – USD FOB

NEW CROP PRICES ARE BASED ON TRACK BID/OFFER SPREAD PLUS ACCUMULATION & FOBBING COSTS AND ARE NOT FOB PRICE INDICATIONS

Australian Grains & Oil Seed Market

Australian domestic grain markets saw little change for the most part last week. Farmer selling has been steady into export destinations but for the most part, farmers are doing fieldwork ahead of the new growing season. In the drier region, farmers are starting to dry plant, and remain reluctant sellers. There is limited urgency however as domestic feedlots will eventually come to market to support price expectations away from export markets.

As previously reported, Barley is firmer following the announcement that China will review its position on Australian barley imports. This has stalled farmer selling. Traders edged prices higher when the China review was first announced but it will be some months before the review is complete. Traders will now be reluctant about pushing prices without confirmed demand and with the Islamic world celebrating the end of Ramadan the markets of the Middle East were very quiet.

There is little buyer urgency to be seen in a global market that is comfortable enough in the old crop and seemingly no major weather concerns for the 2023/24 season. This leaves the reasons for old crop price support to shorts, local weather and the Russian floor price. Thus, export sellers are starting to lower their price expectations.

Feed wheat was sold into the Philippines late in the week at around $293 c&f for a July/Aug shipment. The wheat is expected to be sourced from Australia. This will work back to a Western Australia FOB price of about $275 FOB compared to the IGC’s ASW weekly quote of $301 FOB. Prices still comfortably fit back into the farmer bids although exporters continue to give up margin to get the sales on.

Australia exported 3,050,336 tonnes (MT) of wheat in February, down 6 percent from the 3,251,260MT shipped in January, according to the latest data from the Australian Bureau of Statistics. The February 2023 figure is up 13pc from the 2,695,173MT shipped in February 2022.

In containerised exports, Vietnam, China then Thailand were the biggest markets for wheat shipped in February this year on 74,073MT, 59,288MT and 24,983MT respectively.

In bulk sales, China, Thailand then Vietnam were the biggest markets on 652,888MT, 301,776MT and 295,452MT respectively.

Ocean Freight Market & Export Stem

The past week has seen the freight market fluctuate. A widespread improvement in physical indices from Panamax to Handymax has not really resulted in any perceptible changes in fixture rates. There is a large component of the indices finding the correct level having lagged over the previous seven days and the start of the week shows spot levels are still largely below month-to-date figures. There doesn’t appear to be a widespread influx of cargoes to push the demand side of the equation. Operators are all pushing increased forward numbers as expectation builds ahead of a firm end to Q2 and more positivity in Q3.

It was another strong week for shipping stem. There was 720KMT of wheat added to the stem in the past week with 450KMT or 62% of that coming from Western Australia. New South Wales was the next largest of the wheat additions with 110KMT. There was also 80KMT of barley added in Western Australia as well as 93KMT of canola. All up, Western Australia accounted for 58% of the total grain, canola and pulse additions for the week. There was also 55KMT of canola put on the stem into Newcastle in two handy size vessels.

Pulses Market Update

South Australia added more pulses to the stem than grains over the past week as export sales continue. This included 74KMT of lentils and 36KMT of faba beans while there was only 70KMT of wheat put on the stem. Growers still hold significant tonnage on farm for pulses, especially in the southern markets. With the timely rain and subsequent breaks for planting seen over the past two weeks, farmers have seen downward pressure on prices and are happy to release their current season stock to clear the pathway for the new season.

Pulse production in Australia has grown significantly in recent years, driven by increased demand for plant-based protein and a growing global population. In 2022/23, Australia produced approximately 2.2 million tonnes of pulses, up from 1.9 million tonnes in 2021/22. Chickpea production has been particularly strong, with production increasing to 1.4 million tonnes. Lentil production has also increased steadily in recent years, with production reaching approximately 400,000 tonnes.

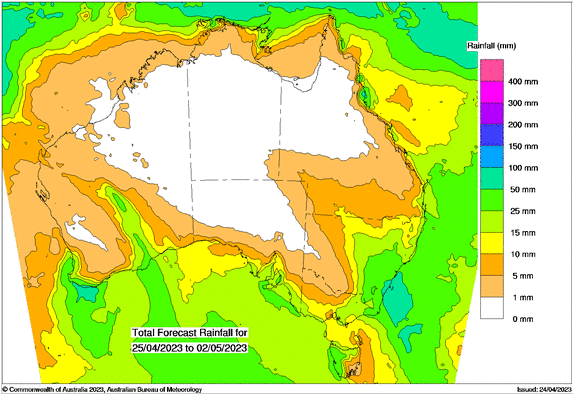

Australian Weather

Most of Australian southern cropping zones have received a timely autumn break and are busily planting pulses and canola following last week’s general rain. Remnants of the Severe Tropical Cyclone Lisa worked its way across Australia’s interior, resulting in some handy rain for South Australia, Victoria in southern New South Wales last week. Most of south-eastern Australia has seen reasonable April rain in recent weeks and this has triggered a general start to winter crop planting.

Farmers were already planting pulses ahead of the weekend rain and are now into canola with wheat and barley to follow. Last week’s dry weather allowed southern farmers to make some considerable planting progress. More rain is needed across north western New South Wales and south western Queensland after a dry April. Topsoils have dried out and the dust is starting to blow across the western Darling Downs and north western New South Wales. Farmers are looking for rain to plant barley and canola in some areas. Farmers in north western New South Wales are already preparing to start dry planting winter crops in the absence of rain. Good subsoil moisture reserves left over from last year’s wet spring will make the decision to start dry planting a little easier. Weather forecasts for the next week are mostly dry.

AUD – Australian Dollar

The Australian dollar was slightly stronger at the close of last week when valued against the USD. The AUD had been under pressure through the week, bottoming during one European session at 0.6678, the lowest level since April 12. For the time being there is no clear direction, and the AUD could trade in a relatively broad range of 0.6620/0.6785.

The post Basis Commodities – Australian Crop Update – Week 18, 2023 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.