Australian Crop Update – Week 45

Harvest and Weather Update

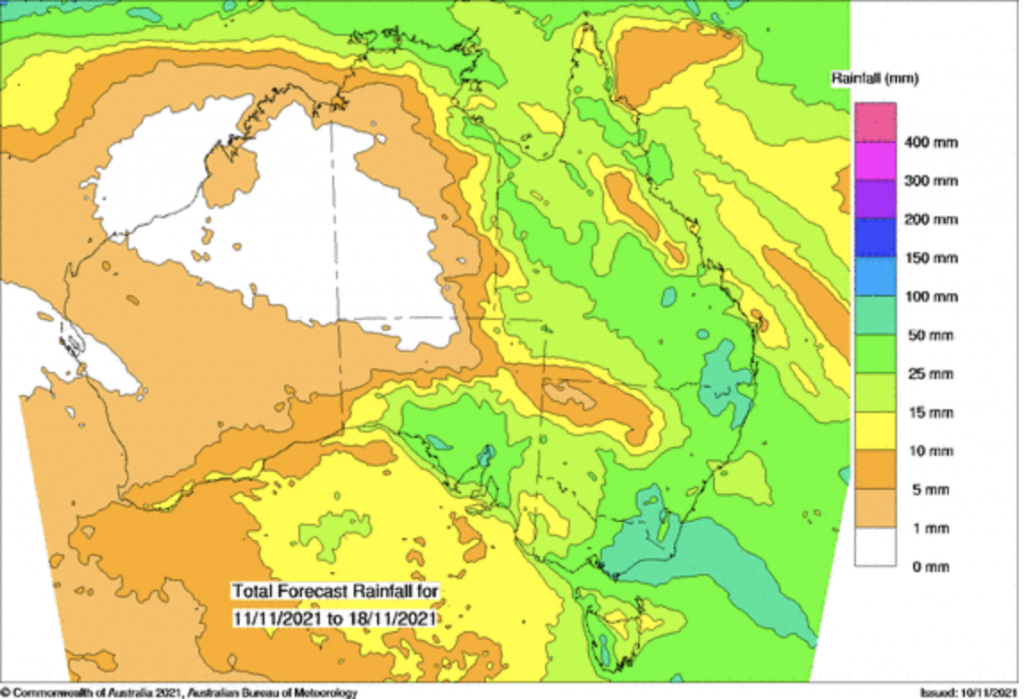

East coast milling quality wheat and ASX futures have moved significantly higher this week as we start to endure the second significant rain system in a week. South Australia and Western Australia also moved higher as a relative value response to east coast values rising. Overnight, storms in Western Australia’s Geraldton zone will stall harvest activity while the east coast and South Australia are waiting to see what’s happens with the forecast torrential rains.

The only saving grace is farmers have made reasonable harvest progress in Northern New South Wales and Southern Queensland, and much of the rest of the east coast, South Australia and Western Australia are still a little away from harvest. In addition, overnight runs of the BOM’s ACCESS model have significantly reduced the volume of rain forecast and have offered an improved vision of the weather for next week – let’s see.

AGsc Australian Balance Sheet Update

Australia’s 2020/21 export program was bought to a close at 23.8MMT and barley was around 7.8MMT. Our analysts updated the balance sheets late last week to reflect the final 2020/21 carry out based on ABS exports. This increase lifts Australia’s 2020/21 wheat production forecast to 34.0MMT and barley production to 13.75MMT.

In terms of 2021/22, forecast rain in the southern half of the country has seen our analysts raise their production forecasts 5% to just under 33MMT for wheat and 12MMT for barley.

Ocean Freight

We have had a more volatile couple of weeks in the bulk freight market. As soon as charterers got a feel that a widespread correction was in play, they all disappeared from the market and we have been left with something of a vacuum. There were some signs of support appearing back in the market this week.

Currency

The Australian dollar faced headwinds, dropping 1.7% for the week as both the RBA and offshore central banks provided more dovish stances to potential interest rate hikes compared to market consensus. In addition, China continues to pursue a COVID policy that has hampered Q3 and Q4 growth expectations. Concerns around the health of the Chinese property market also continue to grow. As such the AUD as a proxy to Chinese growth prospects remains vulnerable to further weakness.

USDA Report Summary

Changes to the wheat numbers played second fiddle to soybeans and corn, where much of the pre-report activity was focused. Globally, USDA lifted Russian wheat production by 2.0MMT to 74.5MMT adding to its very volatile year for them where the USDA has issued both the highest and lowest production estimates of any of the Russian privates or other reputable forecasters. Ukraine’s wheat exports were increased by 0.5MMT to 24.0MMT. EU wheat exports were raised by 1.0MMT to 36.5MMT. Australian 2021/22 exports were unchanged at 23.5MMT but the 2020/21 numbers were raised by 0.5MMT to 24.5MMT. India’s exports were increased by 1MMT to 5.0MMT. Global wheat imports were raised by 3.6MMT to 203.2MMT. Algeria was increased by 0.5MMT to 7.5MMT and Iran up by 1.0MMT to 5.5MMT, Turkey was +1.0MMT to 11.0MMT and Saudi was up by 0.5MMT to 3.5MMT.

World barley production was lowered by 1.8MMT to 146.2MMT, down 14.3MMT on last year. Global imports were unchanged at 33.6MMT but there were some notable changes. Saudi imports were lowered by 0.5MMT to 6.5MMT, Turkey was increased by 0.4MMT to 2.7MMT and China imports were raised by 1.5MMT to 11.1MMT

To receive this information directly to your inbox as soon as it’s released, sign up for our newsletter below.

The post Australian Crop Update – Week 45 appeared first on Basis Commodities.

Share This Article

Other articles you may like

Sign Up

Enter your email address below to sign up to the Basis Commodities newsletter.